Credit scores are a big deal in the United States.

Whether you’re new to the US or have been living here for awhile now, you’ve most likely heard this already.

However, it’s not always clear how or why credit scores are so important, even for many Americans.

That’s why we’re going to go over everything you need to know about credit scores in the US, including how you can start building your credit as an immigrant in the US, no matter how long you’ve been here.

Let’s get started with the basics!

What is a credit score?

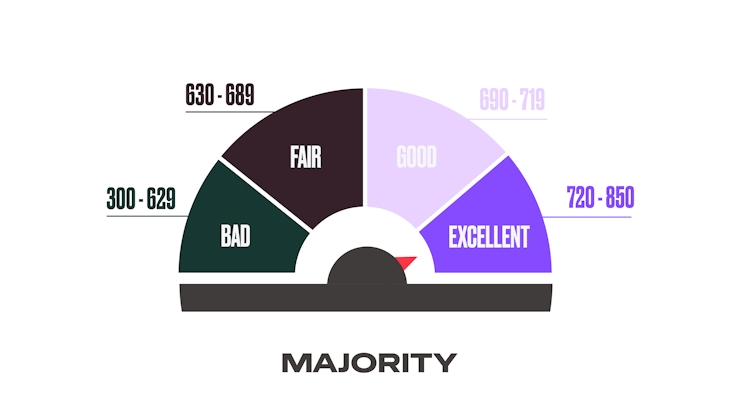

A credit score is a number between 300–850 that determines how creditworthy you are. The higher your score, the more likely you are to receive credit from lenders. On the other hand, a low credit score is a warning sign to lenders that you may not be reliable enough to pay back your debts.

Your credit score is largely based on the length of your credit history, number of loans or lines of credit, repayment history, total amount of debt, and the percentage of available credit you’re currently using.

The FICO score is the most common scoring system used by the largest number of financial institutions.

Is the US the only country with credit scores?

No! It is a myth that America is the only country to use credit scores. However, it is the only one to use the FICO scoring system.

Although credit scoring systems differ around the world, many countries have some system or another set up to automatically track an individual’s creditworthiness. Other countries may also require you to prove your own creditworthiness by showing proof of income, bank statements, and other financial documents when applying for credit.

What affects my credit score?

So the big question is what actually determines if you are creditworthy or not? There are several factors that combined make up your credit score.

These factors have the biggest impact on your credit score.

On-time payments

Perhaps most important is the number of on-time payments you have made on bills and loans. Lenders want to see first and foremost that you’re going to make your payments on-time.

Oldest credit line

Lenders also want to see you have experience handling debt from previous loans and credit cards. This is particularly hard for migrants to have when they’ve just arrived in the country. However, it’s not impossible. More on that later.

Credit used

If you get a credit card, you will have a credit limit, which is how much money you can put on that card. Lenders determine how responsible you are to handle credit by looking at what percentage of your credit limit you have used. The lower the percentage the better.

Recent inquiries

Every time you apply for a loan, a credit credit, or something that requires a credit check, such as filling out an apartment application, it will count on your score as an inquiry. If you have too many inquiries, it will appear as if you are taking on too much debt at once and can feel risky to a lender.

New accounts

If you start too many credit accounts or loans in a short period of time, lenders may interpret this as a sign that you are facing financial hardship. Therefore, it is always a good idea to only get one credit card or loan at a time.

Available credit

The more available credit you have the better! Similar to credit used, this signals to lenders that you are responsible when it comes to borrowing money.

7 Ways to build credit as a new immigrant in the US

The biggest problem migrants face when it comes to building credit in the US is that they have no credit history, and thus no credit score. Therefore, when they apply for a loan or credit card, lenders have no information to base a decision on, which usually ends with them denying your application.

Remember!

No credit score does not mean a good credit score. In most cases, it means the opposite.

But no worries, there are ways for individuals with no credit history to start building credit and get a good credit score. Here are a few simple tips that will help get you started!

1. Apply for a credit card

There are special credit cards that are easier for people with no credit history to get such as “secured” credit cards, store branded cards, and credit-builder cards. These usually have smaller credit limits and higher interest rates. Some may also require a money deposit. How new immigrants can get a credit card is a complex topic of its own, which is why we dedicated a whole article to it here!

2. Find a co-signer

A co-signer is someone who is willing to take responsibility for a loan or credit card payment if you fail to pay on time. However, if you can find a close relative who you can trust and has a good credit score, they can cosign for you when you apply for a credit card or loan, which increases the chances your application is approved.

3. Become an authorized user

If you share finances with someone who already has a credit card, you can become an authorized user on their account. That means you will get your own credit card without having to apply for one on your own. The main user is still responsible for payments, however, which is why this solution is best for spouses or close relatives.

4. Report rent and utilities to credit bureaus

If you are renting and making on-time payments to a landlord, there are special rent reporting services you can use to report your payments to credit bureaus so that you start to build credit. Additionally, you can ask your water, electric, gas, or cable providers if they report your payments so that they also count towards your score.

5. Pay on-time!

The best thing you can do to build credit is to pay on-time. Once you’ve opened a credit card or taken out a loan, you have to prove to lenders that you are reliable, which means paying back what you owe. Remember, once you have a credit score, you have to maintain it, and it can be much more difficult to recover from a bad credit score than to build one from scratch. So once you get started, don’t let your credit score slip by forgetting to make payments. Late payments usually come with an extra fee as well.

6. Don’t use all your credit

As a rule of thumb, you should not use more than 30% of your available credit. For example, if you have one credit card with a credit limit of $1,000, you should not have a balance of more than $300 at any time. To avoid paying pricy interest fees, it’s also a good idea to pya off your balance in full every month.

7. Look out for identity theft

Unfortunately, people just starting to build their credit score can be vulnerable to identity theft. That being said, if you review your credit card statements and other bills every month, you can detect suspicious activity before it’s too late. You should also be careful not to share private information with anyone you don’t trust, especially your Social Security number or ITIN.

The benefits of a good credit score

A good credit score is usually between 690–850. If you can keep your score in this range, you have a much better chance to be approved for credit cards and loans, should you need one. It will be especially helpful when it’s time to make a big purchase like buying a car or house.

Not only are banks and lenders much more likely to approve your application with a good credit score, they will usually offer a much better interest rate as well.

On the other hand, with a bad credit score, you risk being unable to take out a loan or open a credit card. It may also be harder to find a home to rent if a potential landlord wants to run a credit check.

Therefore, it’s worth taking care of your credit score, because you never know when it will come in handy!

It’s time to start building credit!

Now that you have the basics down, you can choose the credit-building method that’s right for you! Although it’s a lot of responsibility, it can also be a lot of fun knowing that you’re building a better financial future for yourself.

And if you found this content useful, check out more of our articles by downloading the MAJORITY app or visiting our Community blog where we have tons of advice, tips, and tricks for thriving in the US.

We also specifically help migrants to take their money farther by offering an FDIC-insured spend account to keep your money safe with no overdraft, minimum balance, or foreign transaction fees. Plus, your account comes with a Visa® Debit card that gives you exclusive access to discounts in your own community. And these are just some of the effortless ways we help you save. Learn more and get started today!